The Physical and the Social

Infrastructure Proposals — $4 trillion

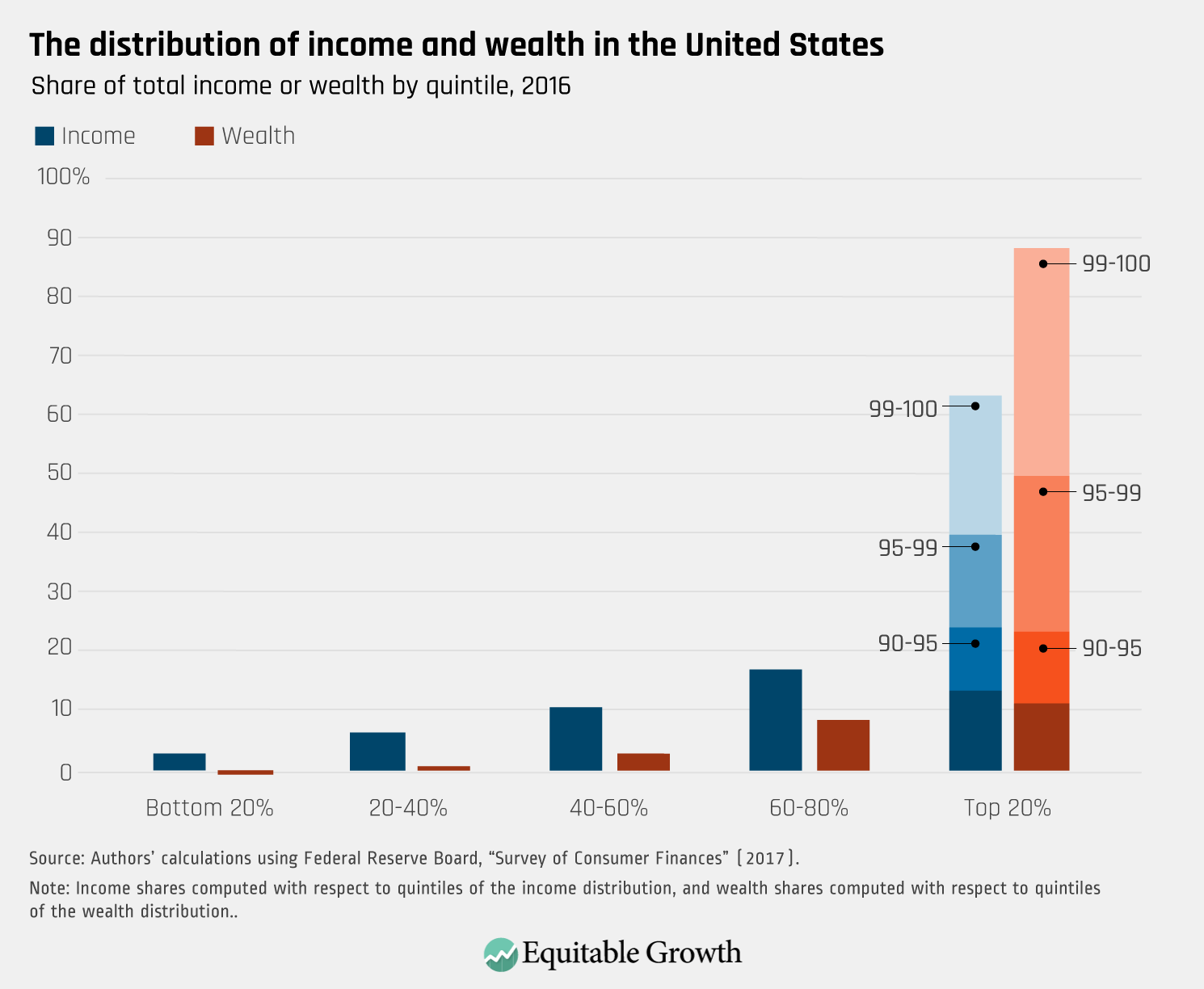

I realize that economics is extremely boring. But would you like to add another $20,000 to your yearly income, and not just your family but all families who earned less than $200,000 last year? Naturally, everyone would like that, but how? Now economics is not so boring. You can look at a web page from the Economic Policy Institute, the Wage Calculator, that answers “What Should You Be Making?” Approximately 90% of families or households have incomes below $200,000. The share of total national income going to the lower 90% was 13% greater in 1980 than today’s share. The 13% shift in total income is a difference of $20,000 to $40,000 for every family earning less than $200,000. The economy grew, definitely, but the benefit went to only a small fraction of families, the top 10% and especially the top 1% and 0.001%.

“The New Gilded Age”, a report from the Economic Policy Institute, finds that between 1973 and 2007 58.7% of income growth “landed in the hands of the top 1 percent of families.” While the incomes of the lower earning 99% increased by 15.4%, the incomes of the top 1% increased by 216.4%. (page 12, pdf version). During the years 1945 to 1973 the reverse was seen, the top 1% received only 4.9% of growth, their incomes grew by 34.3% while the 99% grew their incomes by 100.1%.

From the period 1945 to 1973 all income levels grew more or less at the same rate as the entire economy grew, but then there was a sea change, since 1973 only the top incomes have grown at the same rate as the entire economy’s growth rate. Income growth for the lower 90% was slow to non-existent. That’s me and you. How can we reverse the shift? The Infrastructure plans are a beginning.

Trump tried to address this problem, but he failed, quite simply. The tax cut he passed benefitted high income households (who did not need a cut) much more than middle- and low-income households. Trickle-down doesn’t work. And the majority of jobs created since 1990 have been low-wage jobs paying between $20,000 to $35,000 per year.

We have to start with a bottom-up strategy to achieve shared prosperity. It’s correctly called wage-led growth.

The economy is not working well for about half of the U.S. population, and this should concern everyone.

The United Way since 2009 has published a report on poverty and hardship, the ALICE report (Asset Limited, Income Constrained, Employed). In December, 2020, in its report “On Uneven Ground” it said, “approximately 40% of American families struggle to make ends meet. In 2017, 13% of U.S. households earned below the FPL [Federal Poverty Level], and another 28% were ALICE [a total of 41%] . . . . [They have] income above the FPL but not enough to afford the basic necessities of housing, child care, food, transportation, health care, and a smartphone plan. They live paycheck-to-paycheck. And because they earn above the FPL, they are largely ineligible for public assistance programs.” The conclusion of its report says, “half of all U.S. households could be in poverty or be ALICE by the end of the pandemic.” In 2018 in Mariposa County the ALICE status reached 42% of the population, as reported in the National Overview for that year. ALICE affected 60% of Madera County and 52% of Fresno county.

You can fairly ask what has that to do with infrastructure. The answer: about 4 million decent paying jobs will be created for the full 10 years of the proposal. This will tend to “tighten” the jobs market and raise wage income for all other workers. And the cost of living will decline because of the services provided by the two infrastructure bills.

These bills will employ low income workers. President Biden in his State of the Union message said, “Nearly 90 percent of the infrastructure jobs created in the American Jobs Plan do not require a college degree; 75 percent don’t require an associate’s degree. . . . [It’s] a blue-collar blueprint to build America.”

Though the cost sounds high, $4 trillion (over 10 years), the U.S. private savings, or “household net worth", is $136 trillion. (Flow of Funds, page 2) I am guessing that most readers are just blanking-out at that figure, $136 trillion. Try comparing $4 trillion with $136 trillion. In 2019 the GDP (annual economic product) was around $20 trillion — so $136 trillion is a lot larger, right? There is a lot of private savings, even though my share is a pittance. The ratio of wealth to annual output (GDP) has never been higher; wealth is booming but it benefits only — the rich. Not the ordinary workers who earn less than $200,000 per year. And, to lose most of the readers, total wealth in the U.S. grew by more than $78 trillion over the past 12 years, which is more than $6 trillion per year. The infrastructure cost will be $0.4 trillion per year. It should be obvious, we have an imbalance; the rich are saving too much and the poor are spending too little.

Read this article on the internet: “Want to Expand the Economy? Tax the Rich!” by Nick Hanauer, a multi-millionaire, a serial entrepreneur. Learn that Harley Davidson is making motorcycles in Thailand, and that “Low wages and rising inequality are not symptoms of slow growth; low wages and rising inequality are the disease that cause slow growth — and inequality cannot be cured by creating even more inequality.” (He’s referring to the tax cut bill that benefitted millionaires.) It’s at the American Prospect, Summer 2018.

When the majority of workers cannot afford to purchase the value of what they produce, the result is declining consumption, fewer well-paying jobs, lower income and less savings for the majority. This is a rule of economics that is not going to change. That decline leads to unstable families and unhealthy communities, and public services that are inadequate. We can travel far down the road of inequality before we come to a crisis; Mexico is a bad example of how inequality will destroy the quality of life. But why go down that road? Proposals to reverse this trend desperately need widespread support, including voting support. Fly the American flag with pride, but choose an effective strategy to reverse these impoverishing trends.